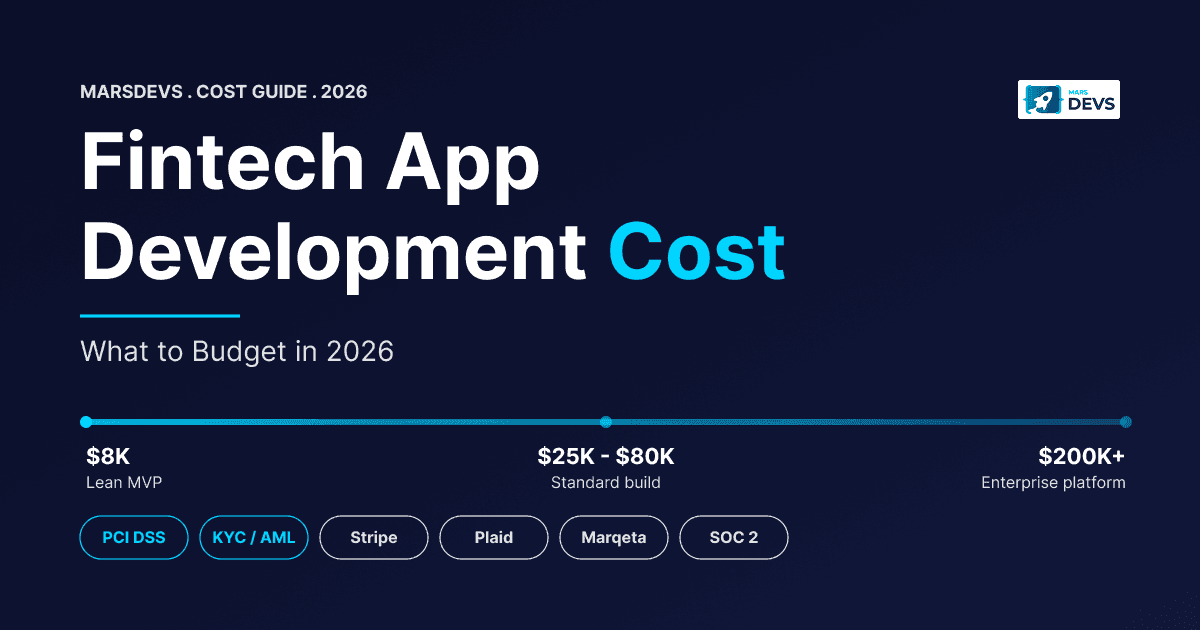

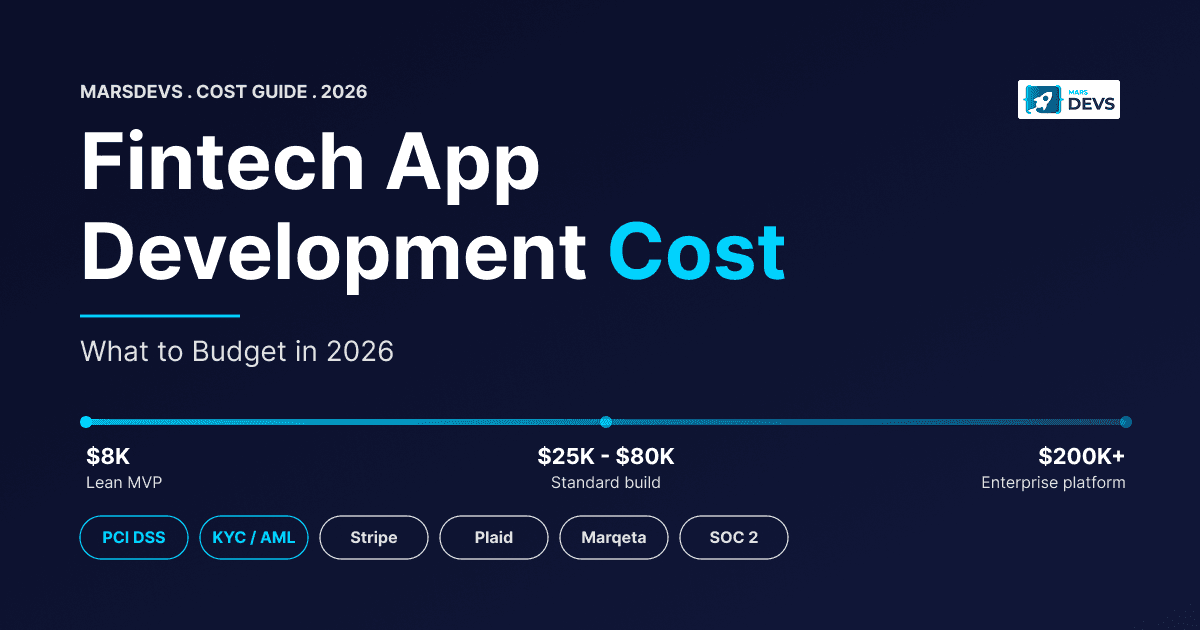

TL;DR: Fintech app development cost in 2026 ranges from $8,000 for a lean payment MVP to $200,000+ for a full neobanking platform. Most fintech startups spend $25,000 to $80,000 on a production-ready first version. The real budget killers are compliance (PCI DSS alone runs $5,000 to $50,000), API integrations ($300 to $3,000/month for Plaid, Stripe, Persona, Marqeta, Sumsub), and ongoing security audits ($15,000 to $25,000/year). MarsDevs has shipped fintech apps at $15 to $25/hour across 12 countries since 2019, covering payments, lending, and KYC pipelines.

Fintech apps cost 2x to 3x more than equivalent SaaS dashboards because regulation and security drive the budget, not features. Founders who plan only for feature work run out of money before launch. PCI DSS, KYC integration, encryption standards, and security audits are the real line items.

You have a fintech idea. Maybe a payment app, a lending platform, or a neobanking tool. You search "fintech app development cost" and find numbers that range from $20,000 to $300,000. That spread is so wide it is useless.

Here's the thing: fintech is not a normal software category. The cost to build a fintech app is driven as much by regulation and security as by features. A payment app with the same feature set as a SaaS dashboard costs 2x to 3x more once you add PCI DSS, KYC integration, encryption standards, and security audits.

The global fintech market hit $460 billion in 2026, according to Fortune Business Insights. That growth pulls thousands of startups into the space every quarter. Most of them underestimate what it actually costs to ship a compliant financial product.

We have shipped 80+ products across 12 countries since 2019. Several of them are live fintech apps: payment tools, lending dashboards, KYC automation pipelines, and treasury workflows. The numbers in this guide come from production projects, not estimates from a pricing calculator. If you are a founder sizing your financial app budget, this is the breakdown you need before you write a single line of code.

For the full development process (not just costs), read our how to build a fintech app guide.

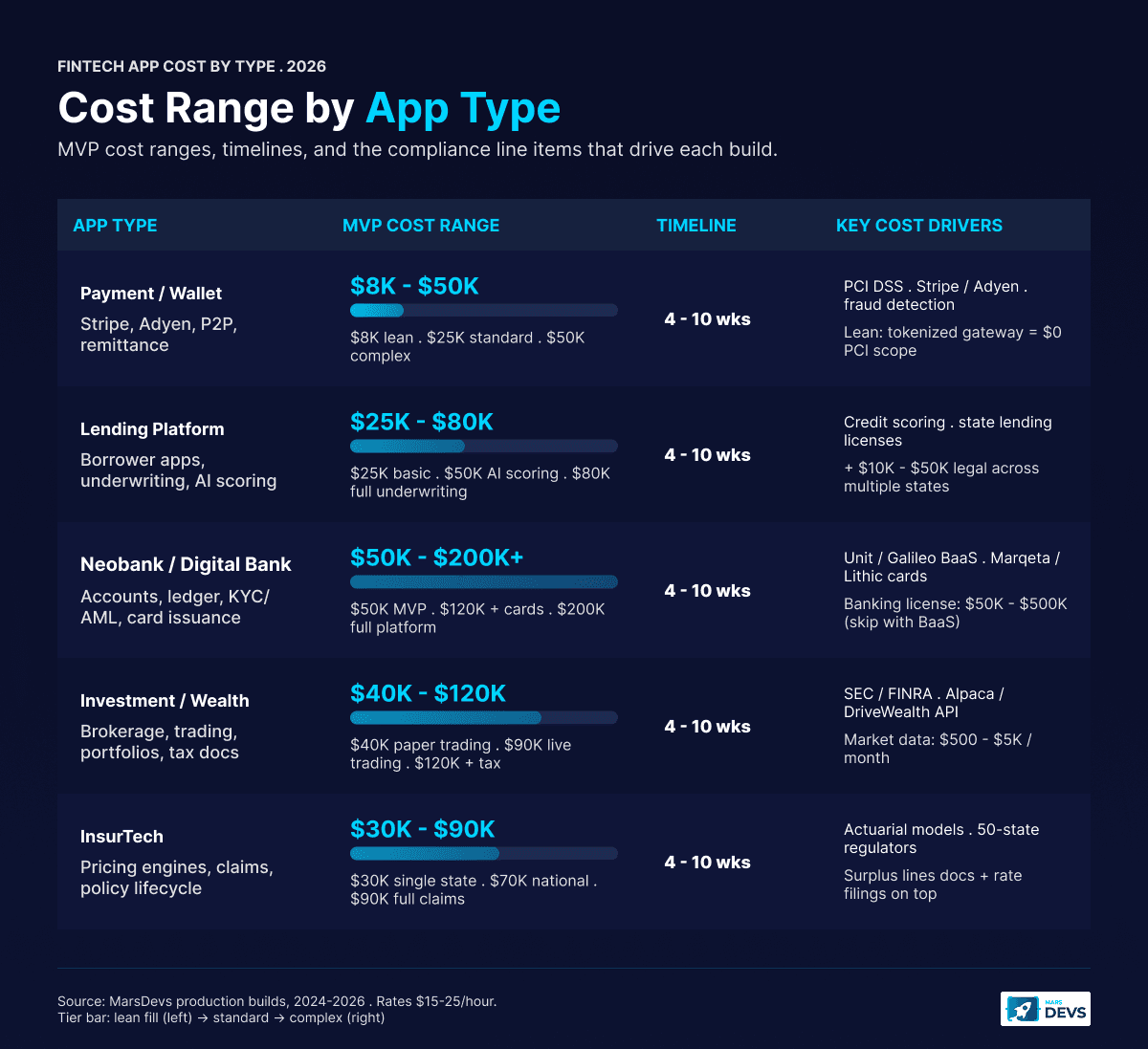

Fintech app development cost varies by category: payment apps run $8,000 to $50,000, lending platforms run $25,000 to $80,000, neobanks run $50,000 to $200,000+, investment apps run $40,000 to $120,000, and insurtech runs $30,000 to $90,000. The compliance burden, integration complexity, and licensing requirements differ dramatically.

Pick the wrong category and you start a startup with the wrong runway. Here is how fintech development pricing breaks down by app type in 2026.

| App Type | MVP Cost Range | Timeline | Key Cost Drivers |

|---|---|---|---|

| Payment/Wallet App | $8,000 to $50,000 | 4 to 10 weeks | PCI DSS, Stripe or Adyen, fraud detection |

| Lending Platform | $25,000 to $80,000 | 6 to 14 weeks | Credit scoring, lending regulations, underwriting |

| Neobank/Digital Bank | $50,000 to $200,000+ | 10 to 20 weeks | Banking partner (Unit, Galileo), ledger design, KYC/AML |

| Investment/Wealth App | $40,000 to $120,000 | 8 to 16 weeks | SEC/FINRA compliance, brokerage API, market data |

| InsurTech | $30,000 to $90,000 | 6 to 12 weeks | Actuarial models, claims processing, state regulations |

Payment apps are the most common entry point for fintech founders. They process transactions between users, merchants, or both. Think Venmo, Cash App, or Wise.

At MarsDevs rates of $15 to $25 per hour, a lean payment MVP with basic send/receive, user authentication, and Stripe integration takes 4 to 6 weeks and costs $8,000 to $20,000. Add PCI DSS scope, fraud detection, and multi-currency support, and you are looking at $30,000 to $50,000. We shipped one such MVP in 5 weeks last year for a US-based remittance founder; total build came in at $18,400.

The cost driver most founders miss: PCI DSS compliance. If your app touches card data directly (not through a tokenized gateway like Stripe), compliance alone adds $5,000 to $20,000 to your development budget and $3,800 to $10,000 annually in maintenance, according to Sprinto.

For a deeper view of how payment costs compare to general SaaS, see our cost to build SaaS guide.

Lending apps connect borrowers with capital. They need credit scoring logic (increasingly AI-powered), regulatory compliance for lending practices, secure data handling, and underwriting workflows. The data architecture is heavier than a payment app because every loan has a lifecycle: application, decision, disbursement, servicing, repayment.

A basic lending MVP costs $25,000 to $40,000 and includes borrower applications, manual credit review, loan tracking, and repayment processing. Add AI credit scoring with alternative data sources, automated underwriting, and risk dashboards, and you reach $60,000 to $80,000.

Lending regulations vary by jurisdiction. If you operate in the US, you need state-by-state lending licenses. That regulatory overhead adds both development cost (jurisdiction-aware logic) and legal cost ($10,000 to $50,000 for licensing across multiple states).

Neobanking is the most expensive fintech category. You need a banking partner (Unit, Galileo, or Synapse-style sponsorship), full KYC/AML compliance, double-entry ledger design, core banking integration, and multi-channel support.

A neobank MVP with account creation, balance management, basic transfers, and KYC onboarding starts at $50,000. Add card issuance through Marqeta or Lithic, bill pay, P2P transfers, and a full compliance dashboard, and you cross $120,000 to $200,000. The banking license or sponsorship alone can cost $50,000 to $500,000 depending on jurisdiction.

This is not where you start if you have less than $200,000 in development budget. Start with a focused payment or lending product, validate your market, then expand into banking. We have watched founders burn through their entire seed round trying to build a full neobank from day one.

Investment apps add a regulatory layer most founders underestimate. SEC and FINRA registration apply the moment you let users buy or hold securities. You also need brokerage API access (Alpaca, DriveWealth, Apex), real-time market data, and audit-grade trade logs.

A wealth MVP with paper trading, watchlists, and read-only portfolio import runs $40,000 to $60,000. Add live trading, real-time order routing, and tax document generation and you cross $90,000 to $120,000. Market data alone adds $500 to $5,000/month at retail-broker scale.

InsurTech sits closer to actuarial science than to traditional fintech. You build pricing engines, claims workflows, and state-by-state policy logic. Most insurtech founders underestimate the cost of adapting to 50 separate state regulators.

A basic insurtech MVP for a single state costs $30,000 to $50,000. National-scale insurtech with claims processing, agent dashboards, and policy lifecycle management runs $70,000 to $90,000. Agent licensing, surplus lines documentation, and rate filings add legal costs on top.

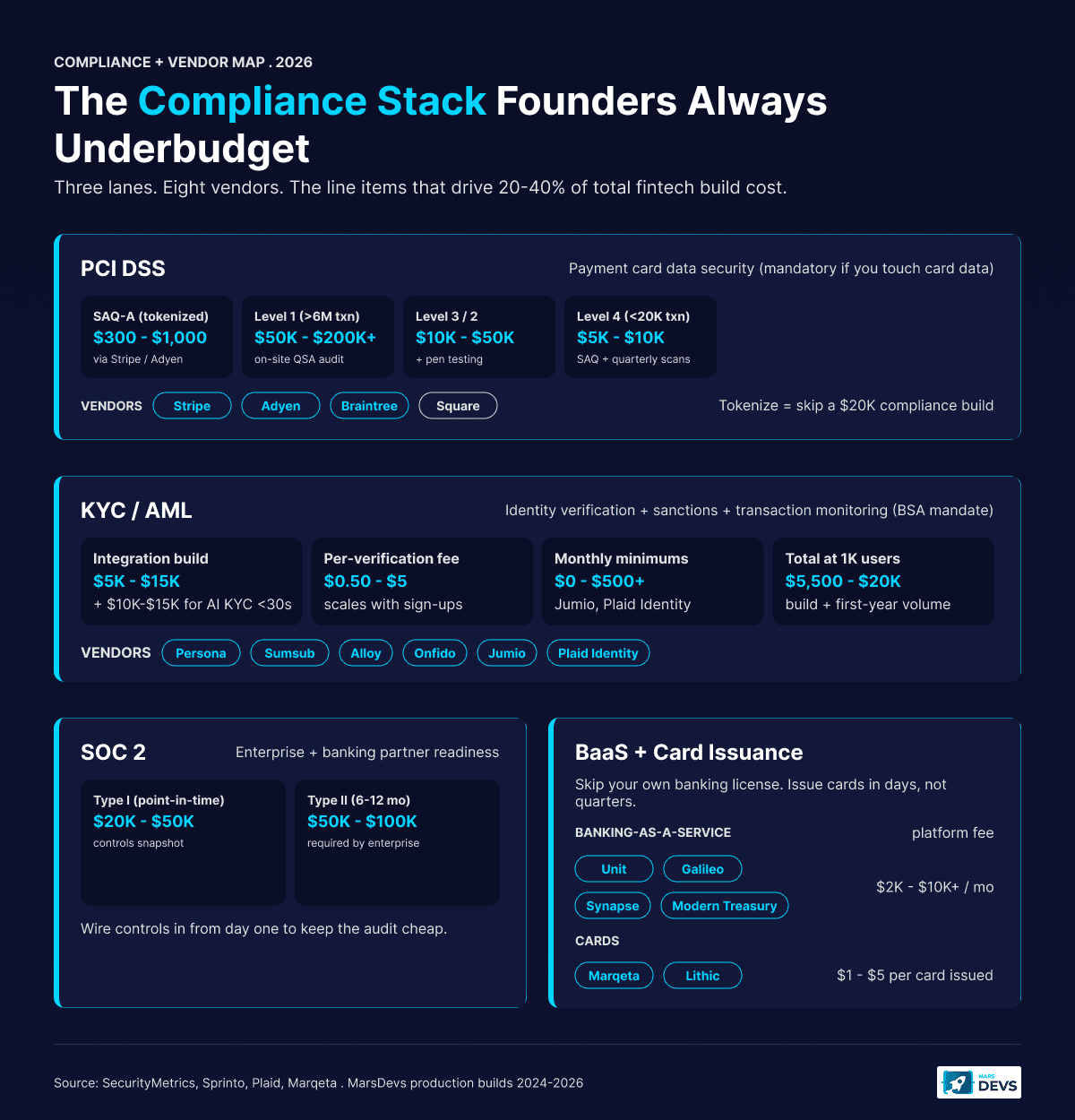

Compliance accounts for 20% to 40% of total fintech development spend. PCI DSS runs $5,000 to $200,000+ depending on transaction volume, KYC/AML integration runs $5,000 to $30,000 plus $0.50 to $5 per verification, and SOC 2 Type II runs $50,000 to $100,000 once enterprise clients demand it. Founders budget for features and design, then discover compliance ate half the budget.

Here is what each compliance layer actually costs in 2026, drawn from active projects.

PCI DSS (Payment Card Industry Data Security Standard) applies to any fintech app that processes, stores, or transmits credit card data. The cost depends on transaction volume and how directly you handle card data. Most early-stage fintechs land at Level 4.

| PCI Level | Annual Transactions | Compliance Cost | Requirements |

|---|---|---|---|

| Level 4 | Under 20,000 | $5,000 to $10,000 | SAQ, quarterly scans |

| Level 3 | 20,000 to 1 million | $10,000 to $25,000 | SAQ, quarterly scans, pen testing |

| Level 2 | 1 to 6 million | $20,000 to $50,000 | SAQ, quarterly scans, pen testing |

| Level 1 | Over 6 million | $50,000 to $200,000+ | On-site audit (QSA), quarterly scans |

The smart move for most startups: use a tokenized payment processor (Stripe, Stripe Connect, Adyen) that handles PCI on their end. Your app never touches raw card data. You fill out an SAQ-A form ($300 to $1,000) instead of a $20,000 compliance build. You pay Stripe's transaction fees (2.9% + $0.30) instead of building PCI infrastructure yourself.

But there's a catch. If your app stores card numbers, manages its own payment vault, or processes transactions directly, you need full PCI scope. That means penetration testing ($15,000 to $25,000/year), vulnerability scanning ($200 per IP annually), and ongoing documentation and training ($3,800 to $10,000/year), according to SecurityMetrics.

Know Your Customer (KYC) and Anti-Money Laundering (AML) compliance is mandatory for any fintech app that handles money transfers, lending, or banking. The Bank Secrecy Act (BSA) sets the floor in the US. You need identity verification, document checks, sanctions screening, and ongoing transaction monitoring.

Most startups integrate a third-party KYC provider rather than building in-house. Here is what the major providers cost in 2026:

Integration development costs $5,000 to $15,000 depending on the provider and how deeply you embed KYC into onboarding. For AI-powered KYC that processes verifications in under 30 seconds (vs. 5 to 15 minutes manually), add another $10,000 to $15,000 for model integration and edge-case testing.

SOC 2 is not legally required for most fintech startups, but enterprise clients and banking partners will demand it. Type I certification (point-in-time) costs $20,000 to $50,000. Type II (ongoing, 6 to 12 month audit period) runs $50,000 to $100,000.

Most early-stage fintechs skip SOC 2 initially and add it when they sign their first enterprise deal or banking partnership. Budget for it in your year-two plan. Every SOC 2 build we have shipped landed under $40,000 because we wired the controls in from day one rather than retrofitting.

If you move money between users, the BSA and state-level money transmitter laws kick in. License fees vary widely. California, New York, and Texas are the expensive ones. Some founders launch under a regulated partner (Modern Treasury, Unit) to avoid direct licensure. That partnership is the single biggest cost saver in early-stage fintech, and we recommend it for almost every payment-adjacent MVP.

Fintech API integrations consume 15% to 20% of total development cost. Stripe charges 2.9% + $0.30 per transaction, Plaid charges $0.40 to $0.90 per active user monthly, Marqeta and Lithic charge $1 to $5 per card issued, and Unit/Galileo BaaS contracts run $2,000 to $10,000+ monthly. Plan for the full multi-year run rate, not just the first month.

Payment processing is the backbone of most fintech apps. Here is what the major gateways charge in 2026:

| Provider | Transaction Fee | Monthly Fee | Integration Cost |

|---|---|---|---|

| Stripe | 2.9% + $0.30 | None | $3,000 to $8,000 |

| Stripe Connect | 2.9% + $0.30 + $2/active account | None | $5,000 to $12,000 |

| Adyen | $0.12 + scheme fees | None (min $120) | $5,000 to $12,000 |

| Square | 2.6% + $0.10 | None | $3,000 to $8,000 |

| PayPal/Braintree | 2.59% + $0.49 | None | $3,000 to $10,000 |

For a fintech processing 10,000 transactions per month at an average of $50 per transaction, Stripe fees alone run about $17,400/month. At scale, negotiating custom rates or moving to Adyen (with lower per-transaction fees) saves thousands monthly. We helped one client cut payment processing from $42,000/month to $28,000/month by switching to Adyen at 80,000+ transactions/month.

Stripe Connect is worth its premium when you run a marketplace. It handles split payments, payouts, and 1099-K reporting. We wired Stripe Connect into a creator-economy fintech in 11 days; building those flows from scratch would have taken 5 weeks.

If your fintech app needs to read bank account data (for budgeting, lending decisions, or account aggregation), you need a banking data API. Plaid is the default. Yodlee and MX are the alternatives.

Plaid charges approximately $0.50 per connected user per month on its pay-as-you-go plan, with entry-level plans starting at $500/month for up to 1,000 users, according to Plaid's pricing page. Integration development typically costs $5,000 to $15,000 depending on which Plaid products you use (Transactions, Auth, Identity, Balance).

At early-stage volumes (5,000 users), expect Plaid costs around $0.90 per active user monthly. At scale (200,000+ users with an enterprise agreement), that drops to approximately $0.40 per user, according to Monetizely's analysis.

If your app issues debit, credit, or prepaid cards, you connect to a card issuer-processor. Marqeta and Lithic are the two most common. Both charge per-card and per-transaction fees, plus a setup commitment.

Expect $1 to $5 per card issued, $0.05 to $0.15 per authorization, and $10,000 to $25,000 in integration cost. Lithic moves faster for early-stage builds. Marqeta is the choice once you scale into enterprise issuance volumes.

Banking-as-a-Service (BaaS) providers compress months of bank-partnership work into an API. Unit and Galileo handle account creation, ledger management, and money movement. Modern Treasury sits one layer above and orchestrates ACH, wires, and reconciliation across multiple banks.

BaaS pricing is mostly contractual: monthly platform fees of $2,000 to $10,000+, plus per-account and per-transaction charges. Integration runs $15,000 to $40,000. The math works once you have 1,000+ accounts. Below that, you are paying for capacity you do not use.

Budget 15% to 20% of your total development cost for API integrations. For a $50,000 fintech build, that is $7,500 to $10,000 just for connecting to external services. Underbudget here and you will rebuild integrations 6 months in.

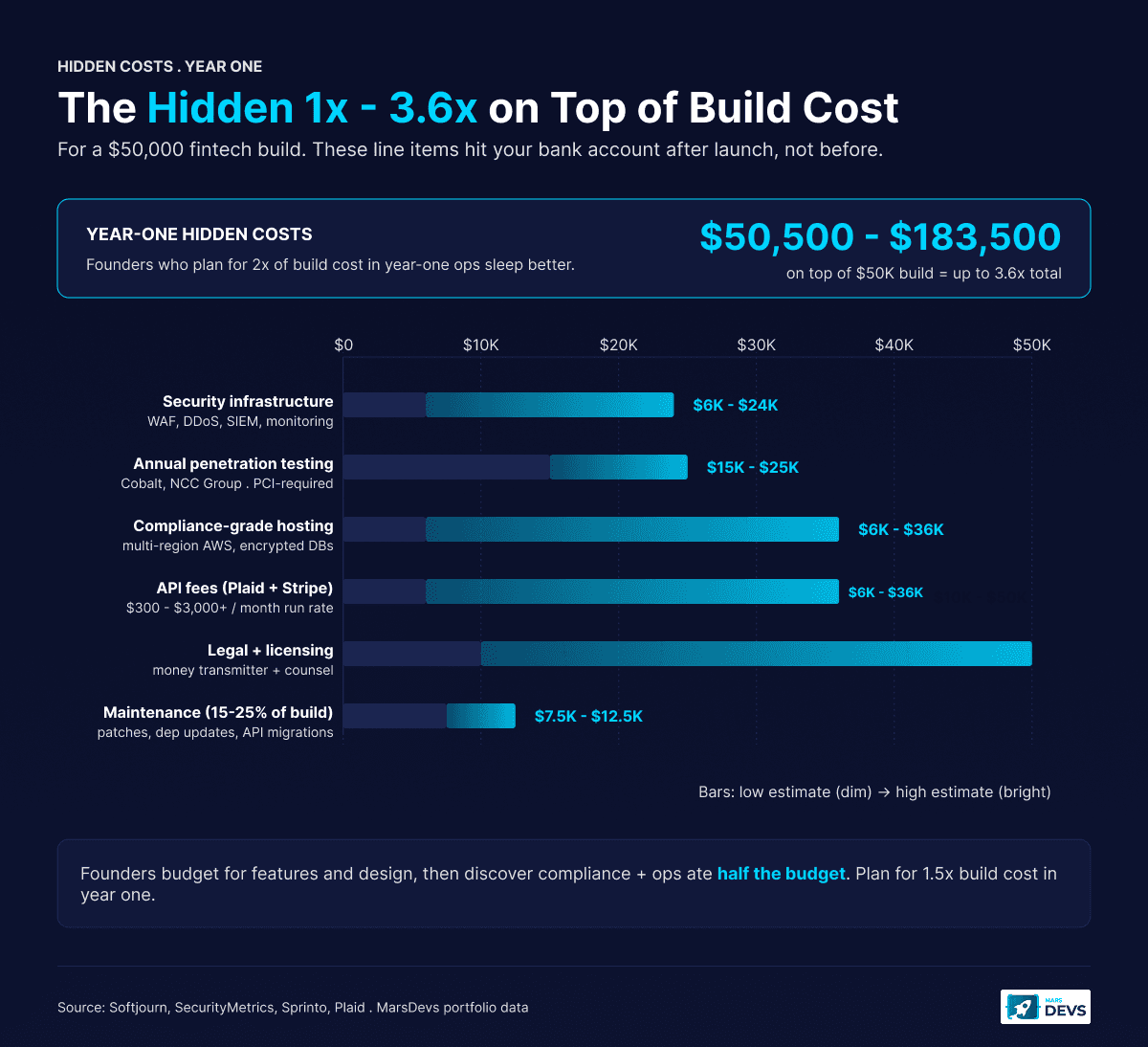

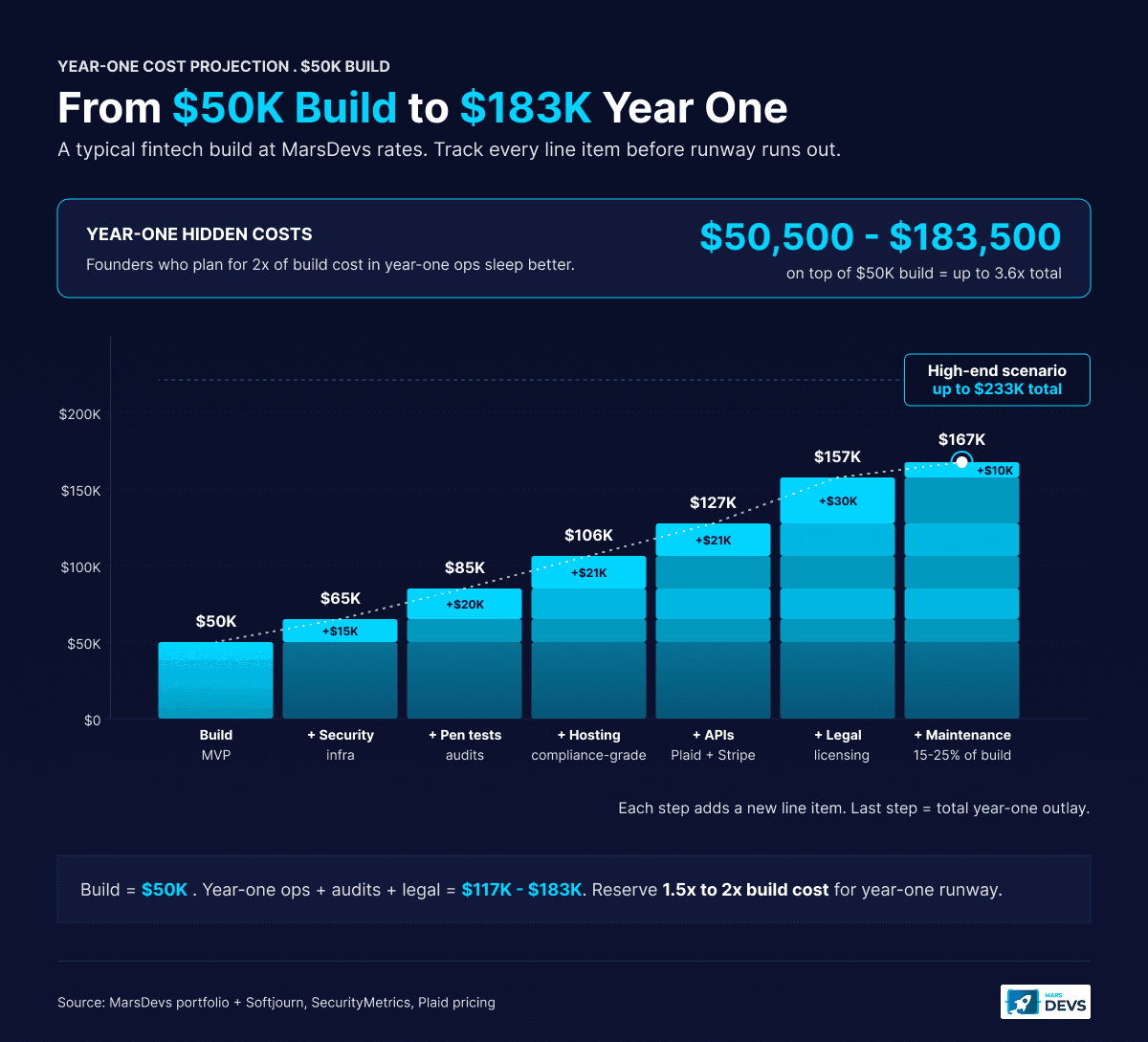

Hidden fintech costs run $50,500 to $183,500 in year one for a $50,000 build. That is potentially 1x to 3.6x your original development cost. The line items: security infrastructure ($500 to $5,000/month), penetration testing ($15,000 to $25,000/year), compliance-grade hosting ($500 to $3,000/month), API fees, legal/licensing, and ongoing maintenance (15% to 25% of build cost annually).

Every fintech founder we have worked with has been surprised by at least one cost they did not budget for. Plan for them now.

Fintech apps need security layers that standard apps do not: Web Application Firewall (WAF), DDoS protection, intrusion detection, log monitoring, and encrypted data storage. AWS WAF costs $5 per rule per month plus $0.60 per million requests. CloudFlare's business plan (with WAF) runs $200/month. Full security monitoring with Datadog or PagerDuty adds $500 to $2,000/month.

PCI DSS and most banking partners require annual penetration testing from a certified third party. This is not optional. A single deep audit costs $15,000 to $25,000 from firms like Cobalt or NCC Group. Quarterly vulnerability scans add another $800 to $2,400/year.

We schedule pen tests in week 12 of every fintech build, before production launch, then again at month 9. That cadence catches drift early. Skipping the second test is the most common founder mistake we see.

Fintech apps need more infrastructure than typical SaaS products. Multi-region redundancy (for uptime requirements), encrypted databases, isolated VPCs, and compliance-ready logging push hosting costs above standard cloud pricing. A fintech app on AWS typically costs $800 to $2,000/month at early stage, scaling to $3,000 to $10,000/month as transaction volume grows.

Money transmitter licenses in the US cost $2,000 to $50,000 per state, and you may need multiple state licenses before launching nationally. A fintech-specialized attorney charges $300 to $600/hour. Budget $10,000 to $30,000 for initial legal review, licensing applications, and compliance documentation.

If you launch under a regulated partner (Modern Treasury, Unit) instead of pursuing direct licensure, your legal costs drop to $5,000 to $15,000 in year one. The trade-off is a revenue share or platform fee. Run the math at your projected volume; the partnership is almost always cheaper for the first 12 to 18 months.

Post-launch maintenance for fintech apps runs 15% to 25% of the initial development cost annually, according to Softjourn's analysis. For a $50,000 build, that is $7,500 to $12,500 per year covering bug fixes, OS updates, dependency patches, API version migrations, and compliance updates.

Here is what the first year of hidden costs looks like for a typical $50,000 fintech build:

| Hidden Cost | Annual Estimate |

|---|---|

| Security infrastructure | $6,000 to $24,000 |

| Penetration testing | $15,000 to $25,000 |

| Hosting (compliance-grade) | $6,000 to $36,000 |

| API fees (Plaid + Stripe) | $6,000 to $36,000 |

| Legal and licensing | $10,000 to $50,000 |

| Maintenance (15-25%) | $7,500 to $12,500 |

| Total Year-One Hidden Costs | $50,500 to $183,500 |

That is potentially 1x to 3.6x your original build cost. Budget for at least 1.5x your development cost in first-year operational expenses. Founders who plan for 2x sleep better.

A lean fintech MVP ships for $8,000 to $25,000 in 4 to 6 weeks if you follow six rules: tokenize payments through Stripe (zero PCI scope), launch in one jurisdiction, integrate off-the-shelf KYC (Persona, Sumsub, or Onfido), launch under a banking partner like Modern Treasury or Unit instead of pursuing your own license, scope to one core transaction, and partner with a team that has shipped fintech before.

We have shipped 80+ products, and the pattern is consistent: founders who scope aggressively and start lean spend less overall because they validate before scaling.

Skip PCI DSS scope entirely by using Stripe, Stripe Connect, or Adyen for all payment processing. Your app never touches raw card data. You fill out an SAQ-A form ($300 to $1,000) instead of a $20,000 compliance build. This single decision saves most fintech startups $10,000 to $40,000.

Do not build multi-state or multi-country compliance from day one. Launch in one market, validate your product, then expand. Each additional jurisdiction adds $5,000 to $30,000 in licensing and compliance costs. We have watched founders try to launch nationally on day one and burn 6 months on legal alone.

Integrate Persona, Sumsub, or Onfido at $0.50 to $3 per verification instead of building custom KYC. At 1,000 users, that is $500 to $3,000 total. Custom-built KYC with the same accuracy and the same fraud signal would cost $30,000+ to develop.

Modern Treasury, Unit, and Galileo will issue accounts, move money, and handle reconciliation under their license. You skip 12 to 18 months of regulatory work and most of the legal cost. Once you hit product-market fit, you can decide whether to pursue direct licensure.

Cut features aggressively. Your fintech MVP needs:

It does not need (yet): multi-currency, advanced analytics, AI fraud detection, social features, investment portfolio tools, or a full compliance dashboard. Add those after 100 paying users tell you which one matters.

A general-purpose dev agency will build your features. A team with fintech experience will tell you which features to skip, which compliance shortcuts are safe, and how to architect for regulatory expansion later. That second conversation saves more money than any line of code.

We provide senior engineering teams for founders who need to ship fast without compromising quality. At $15 to $25 per hour, a lean fintech MVP costs $8,000 to $25,000 and ships in 4 to 8 weeks. That includes compliance-ready architecture, so you are not rebuilding when you scale.

For a detailed walkthrough of the entire process, see our how to build a fintech app guide. For broader MVP cost benchmarks, see our MVP development cost guide. For mobile-specific costs, check our mobile app development cost breakdown.

| Tier | Cost | Timeline | What You Get |

|---|---|---|---|

| Lean Fintech MVP | $8,000 to $25,000 | 4 to 6 weeks | Core transaction, Stripe integration, basic KYC, user auth |

| Standard Fintech App | $25,000 to $80,000 | 6 to 12 weeks | Multiple transaction types, AI features, compliance dashboard, admin panel |

| Complex Fintech Platform | $80,000 to $200,000 | 12 to 20 weeks | Multi-product, custom compliance, banking API integrations, analytics |

100% code ownership from day one. No vendor lock-in. Start building in 48 hours.

Three scope decisions account for an 8x cost spread: number of jurisdictions (1 vs. 50 states is a 4x difference), number of integrations (3 vs. 10 APIs is a 2.5x difference), and licensure path (BaaS partner vs. direct money transmitter is a 5x difference). The answer almost never lives in the feature list. It lives in scope assumptions.

Founders who say "we want to launch nationally with 8 integrations and our own license" are quoting themselves into a $200,000 build whether they realize it or not.

We start every fintech engagement with a 90-minute scoping call to expose those decisions. Half the time, the founder picks the leaner path once they see the math. For broader stack decisions that affect cost, see our best tech stack for startups in 2026 guide.

US senior fintech developers charge $150 to $250/hour, Western Europe runs $100 to $180/hour, Eastern Europe runs $50 to $90/hour, Latin America runs $40 to $80/hour, and India (MarsDevs) runs $15 to $25/hour. Geography accounts for the single largest variable in fintech development cost. The same scope quoted in San Francisco, London, Berlin, and Bangalore lands at four different numbers.

| Region | Senior Developer Rate | $50K-Build Equivalent |

|---|---|---|

| US (SF, NYC) | $150 to $250/hour | $300,000 to $500,000 |

| Western Europe | $100 to $180/hour | $200,000 to $360,000 |

| Eastern Europe | $50 to $90/hour | $100,000 to $180,000 |

| Latin America | $40 to $80/hour | $80,000 to $160,000 |

| India (MarsDevs) | $15 to $25/hour | $30,000 to $50,000 |

Lower rates do not mean lower quality. Quality is correlated with team experience and process, not zip code. The mistake to avoid: hiring the cheapest team that has never shipped a fintech app. Compliance mistakes from inexperienced teams cost far more than the savings from lower hourly rates. We have done cleanup on three fintech builds in 2025 alone where the original team skipped KYC retention rules. Each rebuild ran $40,000 to $90,000.

For a deeper view of global rate benchmarks, see our global developer rates 2026 guide.

A lean fintech MVP ships in 4 to 6 weeks, a standard fintech app with 4 to 6 integrations ships in 6 to 12 weeks, and a complex BaaS-backed multi-product platform ships in 14 to 24 calendar weeks. Timeline is a lever, not a constraint. The killer is unclear scope, which silently doubles every estimate.

| Scope | Engineering Weeks | Calendar Weeks | Why |

|---|---|---|---|

| Lean payment MVP (Stripe, basic KYC) | 4 to 6 | 4 to 6 | Off-the-shelf integrations only |

| Standard fintech (multi-transaction, dashboard) | 6 to 12 | 6 to 12 | Custom logic + 4 to 6 integrations |

| Complex fintech (BaaS, ledger, multi-product) | 12 to 20 | 14 to 24 | BaaS contracts, multi-state legal, audit prep |

We start every engagement within 48 hours. The first sprint is always integration scaffolding (Stripe, Plaid, KYC) so we know within week 1 whether any third-party blocker will slip the timeline. That early-warning step has saved every fintech project we have shipped at least 2 weeks of compounded delay.

The cheapest way to build a fintech app is a lean MVP at $8,000 to $25,000 that uses tokenized payments (Stripe or Adyen) to skip PCI DSS scope, integrates off-the-shelf KYC (Persona, Sumsub, or Onfido), and launches in a single jurisdiction. At MarsDevs rates of $15 to $25/hour, this approach ships in 4 to 6 weeks. See our how to build a fintech app guide.

PCI DSS compliance costs $5,000 to $200,000+ per year. Startups under 20,000 transactions (Level 4) pay $5,000 to $10,000. Tokenized processors like Stripe drop scope to SAQ-A ($300 to $1,000). Level 1 compliance for apps over 6 million transactions requires an on-site QSA audit and runs $50,000 to $200,000+.

Ongoing fintech costs include maintenance (15% to 25% of build cost yearly), API fees ($300 to $3,000+/month for Plaid, Stripe, Persona), security infrastructure ($500 to $5,000/month), annual pen testing ($15,000 to $25,000), compliance hosting ($500 to $3,000/month), and licensing renewals ($5,000 to $30,000/year). For a $50,000 build, budget $50,000 to $180,000 in year-one operating costs.

KYC integration costs $5,000 to $30,000 in development plus $0.50 to $5 per verification. Persona charges $1.50 to $3 per check, Onfido charges $1 to $5, Sumsub charges $0.50 to $2 at scale, and Plaid Identity Verification starts at $500/month. AI-powered KYC under 30 seconds adds $10,000 to $15,000 in dev cost.

Yes. Offshore fintech development costs 2x to 4x less than US or Western European rates. US senior developers charge $150 to $250/hour. MarsDevs (India, 80+ shipped products across 12 countries) charges $15 to $25/hour. A $300,000 US build equates to $30,000 to $80,000 with us. Choose teams with actual fintech experience, not just cheap rates.

A lean fintech MVP ships in 4 to 8 weeks, a standard fintech app with 4 to 6 integrations ships in 6 to 14 weeks, and a full neobank or multi-product platform takes 12 to 20+ weeks. PCI DSS adds 2 to 4 weeks. MarsDevs starts builds within 48 hours and ships fintech MVPs in as little as 4 weeks.

The default 2026 production fintech stack is React or Next.js for web, React Native or Flutter for mobile, Node.js or Python for backend, PostgreSQL for the database, Redis for caching, and Apache Kafka for event streaming. For fraud detection or credit scoring, add Python with TensorFlow or PyTorch. Stack choice swings cost 10% to 20%; architecture and compliance swing it 50% or more.

Add SOC 2 when enterprise clients or banking partners demand it, usually in year two. Type I costs $20,000 to $50,000 (point-in-time controls). Type II costs $50,000 to $100,000 (6 to 12 month audit period). Most early-stage fintechs skip SOC 2 until a customer or partner asks. Wire controls in from day one to keep the eventual audit cheap.

Fintech app development cost is not just about writing code. It is about compliance, integrations, security, and the dozen ongoing expenses that hit your account after launch. Founders who plan for the full cost picture ship successfully. Founders who only budget for development burn through their runway before reaching users.

The fastest path: start with a lean fintech MVP that uses tokenized payments, off-the-shelf KYC, a banking partner instead of your own license, and a single jurisdiction. Validate with real users. Then scale compliance and features based on actual demand.

We have shipped 80+ products across 12 countries since 2019, including fintech apps for payment, lending, and KYC use cases. We build at $15 to $25/hour with senior engineers who understand PCI DSS, KYC integration, BSA, and financial data architecture. You get 100% code ownership and a compliance-ready codebase from day one.

Want to ship your fintech MVP before your runway runs out? Book a free strategy call and get a custom cost estimate in 48 hours.

We take on 4 new projects per month. Claim an engagement slot.

Co-Founder, MarsDevs

Vishvajit started MarsDevs in 2019 to help founders turn ideas into production-grade software. With deep expertise in AI, cloud architecture, and product engineering, he has led the delivery of 80+ software products for clients in 12+ countries.

Get more insights like this

Join founders, CTOs, and engineering leaders who receive our engineering insights weekly. No spam, just actionable technical content.